Theory and practice

If you browse through articles on the Internet, you will mostly find the same advice. Brilliant lists that start with a consolidation loan and end with personal bankruptcy. I have to disappoint you — this is very damaging nonsense that only preys on your situation and I’ll tell you why I think so.

Most of this is SEO-optimized content (i.e. getting the highest search engine position) on financial websites. As it happens, 99 percent of financial sites include links to consolidation loan offerings in the articles about such loans. Of course, if you take out such a loan, they get a commission for it. This is how affiliation works.

You’ve probably already connected the dots yourself and guessed that such content is not created for you and solving your problems in the first place, but to make money for the site owner. It has been, is, and will be the case. While this makes sense in many areas, there is a clear conflict of interest when dealing with debt.

The second issue is the consolidation loan itself — its design and principle do not work in your favor. When you take it out, you turn many different obligations into a single new one. It seems fine, as long as you don’t think about it. Mostly you will get a slightly lower monthly installment, but definitely a higher total cost.

The fact that the full amount of the loan repayment is increasing needs no explanation. However, why is a lower installment bad?

- Debt that is broken into lower installments extends over a longer period of time, and as a result, you pay more interest each month.

- One lower installment goes easier on your pocket, which may cause you to take out another loan.

- The installment has a defined minimum level that significantly limits your ability to deal with your debts, according to the most effective methods.

Repayment according to highest profitability

There are two main methods of dealing with debt. We’ll start with a purely mathematical approach that maximizes your effectiveness in managing your money.

I assume you have a completed summary of your debts that you made based on the previous material. If not, return to it and follow the instructions.

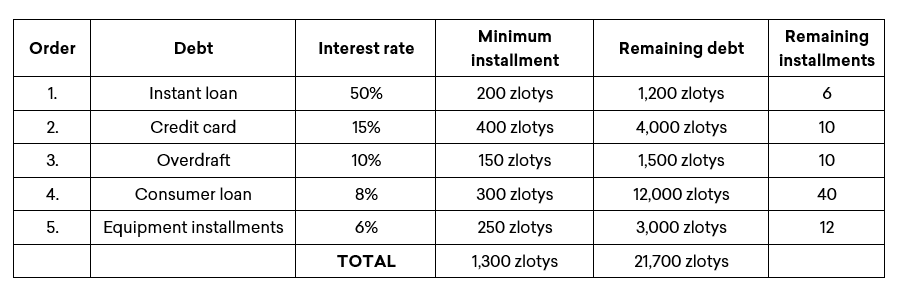

Using the inventory of your obligations in the spreadsheet, sort your debts by annual interest rate. In the case of two debts with identical interest rates, their order is determined by the amount outstanding.

Of course, just arranging your obligations in a certain order doesn’t change anything if you only pay all of them according to the amount of the installment anyway. The method of getting rid of debt only works if you regularly overpay the installments according to a set order. Assuming that the agreement does not provide for extra costs for overpayment, any amount is good — even a few tens of zlotys.

The above table and all calculations are an example of the order of repayments by interest rate. Don’t pay attention to the interest rate with specific products. In reality, they can vary significantly – this is just a simplification.

Your minimum monthly cost is 1,300 zlotys, but after paying bills and other necessary living expenses, you are left with only 1,000 zlotys to pay monthly installments. This means that soon one of your debts will not be paid on time, with unpleasant consequences.

You have several ways out of this situation:

- Pretend there is no problem. Use the folk wisdom of Poles –“it will work out somehow” – sit down and wait for reminders and new acquaintances from the debt collection company.

- Take advantage of payment holiday. If your consumer loan allows you to suspend your payments for, say, 3 months at no additional cost, this is an ad hoc solution. Unfortunately, it does not eliminate the problem.

- Generate additional income. Take overtime or a second job, give private lessons etc.

In the case of earnings deficits, only the last option works. This is a serious situation and in order to avoid falling into a debt spiral that will make your life a nightmare, you need to roll up your sleeves. Payment holiday is just a small help, an option you may not have, depending on your agreement.

Let’s assume that you manage to earn an extra 200 zlotys per month, sell your unused equipment for 400 zlotys at a time and suspend your consumer loan for 5 months. For the next few months the required installments are 1,000 zlotys (until the first debt is paid off) and you now have 1,200 zlotys after paying the minimum installments.

What does tackling the first debt on the list look like?

Amount outstanding – minimum installment – one-time proceeds from the sale of equipment – additional cash at your disposal: 1,200 – 200 – 400 – 200 = 400 zlotys

After the first month there was only 400 zlotys left to repay from the instant loan. You no longer have anything to sell, but you still have an extra 200 zlotys, so the next month you pay off the instant loan to the end.

As of now, you have the amount of 1,200 + 200 zlotys (instant loan installment), and the sum of monthly installments is 800 zlotys (including payment holiday). That means you’ve managed to overpay 1,200 zlotys on your credit card and the source has dried up. At the end of the consumer loan deferment you only have a surplus of 100 zlotys — not bad, but not enough to do much more.

Getting rid of a high-interest instant loan is a good start, but the method has lost momentum, and you’re feeling the gridlock again. While math tells you this is the best solution, emotions work differently.

The snowball method

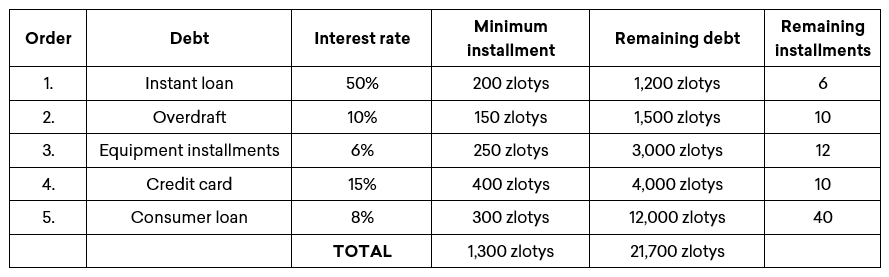

The principle is very similar — we still tackle the debts in a certain order, but this time we change the sorting criterion. We repay in order from the smallest obligation to the largest, without paying attention to interest rates.

Now the summary will look like this:

We stick to the previous assumptions — the sum of installments is 1,300 zlotys, you have 1,000 zlotys each month, but you earn an extra 200 zlotys per month and 400 zlotys one-off, and you take a payment holiday of 5 months for the consumer loan.

It sounds more complicated than it really is.

What does the first month look like?

Amount outstanding – minimum installment – one-time proceeds from the sale of equipment – additional cash at your disposal: 1,200 – 200 – 400 – 200 = 400 zlotys

After the first month there was only 400 zlotys left to repay from the instant loan. You no longer have anything to sell, but you still have an extra 200 zlotys, so the next month you pay off the instant loan to the end.

You have a payment holiday for 3 more months, and the extra 200 zlotys freed up from the instant loan helps you to overpay your overdraft. According to the calculations, in the fifth month (the last one of the payment holiday) you have only 100 zlotys of debt left, and thus 450 zlotys of surplus for the third debt, i.e. equipment installments.

Although the payment holiday ends in the sixth month, there’s not much left of the third obligation, and you’ve freed up much more than the extra 100 zlotys from the first method.

In addition to this, you can see the debts you have already overcome on your list, and this gives you a boost of confidence and faith that you will succeed with the next ones as well. I believe that this is what will happen!

Previous article Checking the situation – inventorying debt